Investing a Roth IRA in early stage growth companies without violating prohibited transaction rules

Given their popularity and widespread use, people rarely think of IRAs as “tax shelters.” But truth be told, that’s exactly what an individual retirement account is: a legal tax shelter.

However, in order to reap the benefits that traditional IRAs and Roth IRAs provide, taxpayers must comply with an assortment of rules. Such rules include limitations on the amount of money that can be contributed to IRAs each year, requirements related to the distribution of assets from those accounts, and restrictions on the types of transactions in which the IRA can engage.

IRAs are also prohibited from making investments into a handful of asset types. Specifically, neither life insurance nor collectibles (stamp collection, classic car collection, Pokémon card collection or similar) can be owned by an IRA. In addition, the S corporation rules prevent IRAs from owning S corporation stock. Other than these three limitations, though, an IRA owner can use the funds within their IRA to invest in any type of asset their heart desires.

Despite the flexibility of permissible investments, most IRA owners stick to more traditional investments, such as stocks, bonds, mutual funds, ETFs, annuities, CDs and other cash equivalents, that can be purchased from or through a traditional financial institution. For a minority of IRA owners, however, the allure of other investment opportunities, such as direct loans, direct purchases of real estate and investments into privately held (non-publicly traded) companies, proves too great to avoid.

For entrepreneurs and business owners, the breadth of assets into which an IRA may invest often gives rise to additional questions like, “How can I shift some of the value of my fast-growing business into my retirement account?” or, “How can I use my IRA to help me start a new business?” And in light of ProPublica’s recent reporting on Peter Thiel’s mind-numbingly large $5 billion Roth IRA, created in large part thanks to his (seemingly) successful efforts to shift the explosive growth of his early stage PayPal and pre-IPO Facebook shares (among many other investments) into his Roth IRA, along with using Roth funds to purchase interests in his Hedge Fund, advisors have already been reporting an uptick in Roth-related questions from clients.

Ultimately, the rules surrounding IRAs make answering the entrepreneur’s questions above exceedingly difficult, due to the complexities of the Prohibited Transaction rules (and the gray areas that exist when trying to push those rules to the limits). In some situations, an IRA owner will have little to no issues with investing some or all of their IRA assets in a business that they also (partially) own and/or in which they work. In other situations, an IRA owner will, quite definitively, be prohibited from making a similar investment. While in still other scenarios, whether or not such an investment would be permissible is a gray area, and largely a calculated judgment of risk vs. reward.

Prohibited transaction limitations for (Roth) IRAs owning small (private) businesses

As noted earlier, in order to enjoy the benefit of IRAs, taxpayers must abide by a variety of rules. One set of rules to which IRA owners must adhere are the Prohibited Transaction rules of IRC Section 4975. The Prohibited Transaction rules restrict an individual from using their IRA to engage in various types of transactions with certain “Disqualified Persons.”

Failing to abide by the Prohibited Transaction rules can land an IRA owner in hot water. Specifically, when an IRA owner causes their own IRA to engage in a Prohibited Transaction, the entire IRA is deemed to be distributed as of January 1 of the year the Prohibited Transaction occurred. Income tax is imposed on the pre-tax portion of the distribution (which is generally the full amount in the case of a traditional IRA, or the growth for a Roth IRA), and if the IRA owner is under 59 ½, the 10% early distribution penalty applies as well. Furthermore, all interest, dividends, and capital gains earned by the investments after the deemed distribution date are considered to be earned in a taxable account, thus further adding to an impacted individual’s tax woes.

IRC Section 4975(c)(1) outlines the various Prohibited Transactions. Specifically, the following types of transactions are prohibited, whether they are engaged in directly or indirectly:

“(A) sale or exchange, or leasing, of any property between a plan and a disqualified person;

(B) lending of money or other extension of credit between a plan and a disqualified person;

(C) furnishing of goods, services, or facilities between a plan and a disqualified person;

(D) transfer to, or use by or for the benefit of, a disqualified person of the income or assets of a plan;

(E) act by a disqualified person who is a fiduciary whereby he deals with the income or assets of a plan in his own interest or for his own account; or

(F) receipt of any consideration for his own personal account by any disqualified person who is a fiduciary from any party dealing with the plan in connection with a transaction involving the income or assets of the plan.”

Notably, a key aspect of the Prohibited Transaction rules is that the enumerated transactions are prohibited regardless of whether or not they are conducted at fair market value. Instead, even if the transaction is conducted for an otherwise bona fide value (akin to what would have been negotiated in an arms-length transaction), the mere fact that the transaction occurs with or for the benefit of a Disqualified Person is still enough to trigger the Prohibited Transaction rules.

An IRA cannot purchase assets from a disqualified person

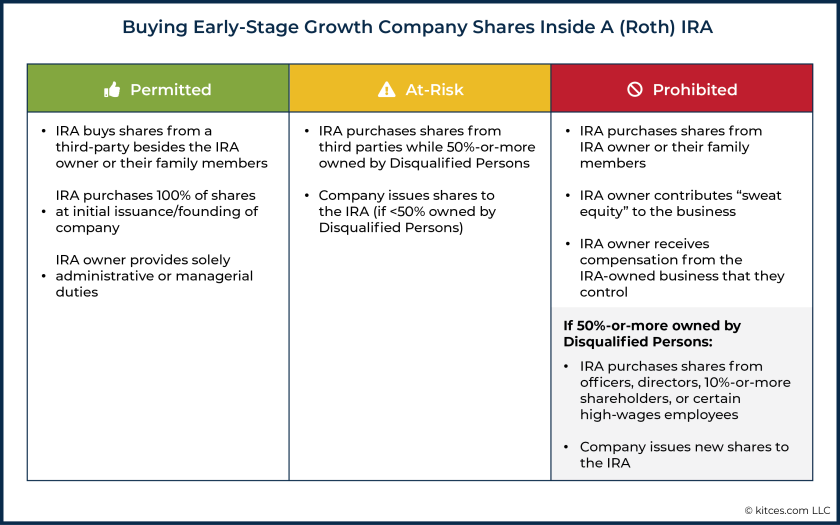

A major challenge for entrepreneurs and business owners looking to invest some or all of their IRA funds into companies they (partially) own is the restriction imposed by IRC Section 4975(c)(1)(A).

More specifically, as described above, IRC Section 4975(c)(1)(A) prohibits an IRA from purchasing property from a “Disqualified Person”.

Disqualified Persons include the following individuals:

- The IRA owner himself/herself

- The IRA owner’s spouse, ancestors, lineal descendants, and any spouse of a lineal descendant.

- An officer or director (or person with similar responsibilities), 10% or more shareholder, or other individual who earns 10% or more of the wages, of a company that is owned 50% or more by the IRA owner and other disqualified persons (combined)

Example #1: Arden is a 10% owner of a rapidly growing business. Her parents each own 10% of the business, while her two children each own 5% of the business. The rest of the business (60%) is owned equally (15% each) by the company’s four officers, who are unrelated to Arden.

Given the projected growth, Arden would like to invest some of her Roth IRA money into the same business (expanding her ownership share using her Roth IRA dollars).

Notably, Arden would not be able to use her Roth IRA to purchase any (of the 40%) of the business that is owned by her parents, her children, or herself directly (as they would all be Disqualified Persons with respect to her Roth IRA). However, since the total ownership of her family members is less than 50%, Arden would be able to purchase additional interests in the company from any of the company’s other shareholders (despite the fact that they are both officers of the company and 10%-or-greater owners).

Notably, because IRAs (and Roth IRAs) themselves can only receive contributions in the form of cash, Arden cannot simply contribute her shares in-kind to her Roth IRA. Instead, the Roth IRA must purchase shares with its own assets in order to own shares. Which means finding another current owner (besides Arden), who is not a disqualified person, and thus would be eligible to sell to Arden’s Roth IRA without triggering a prohibited transaction. Or alternatively, the business would need to issue new shares that Arden’s Roth IRA purchases (with the caveat that the business itself may also be a Disqualified Person!).

Corporations, partnerships and other business entities can also be disqualified ‘persons’

At first glance, the term “Disqualified Persons” might lead one to believe that only individuals – you know, actual human beings – could fall into this category. The reality, however, is that certain entities can also become Disqualified ‘Persons’.

More specifically, if 50% or more of a business is owned by Disqualified Persons, the business itself is also considered a Disqualified Person.

Example #2: Bob and Mary are married, and each own 20% of ABC Inc., a fast-growing tech company. Mary’s mother, Martha, owns another 5% of the company, while their son, Bill, also owns 5%.

Since, in total, Bob, Mary, Martha, and Bill own 50% (via the family attribution rules) of ABC Inc., then ABC Inc. – the entity – would be a Disqualified Person with respect to each of their IRAs. Accordingly, if ABC, Inc. were to issue additional shares of the business, none of their IRAs would be able to purchase those shares.

Because the family attribution rules cause the business, itself, to be a Disqualified Person, issuing new shares to the Roth IRA of any of the family’s Disqualified Persons will create a prohibited transaction. In such situations, only another owner – who is not, themselves, a Disqualified Person by some other relationship to the Roth IRA owner – can be the seller of shares that are transitioned to the Roth IRA.

How to (legally) move shares of an existing business into a Roth IRA

Given the limitations of the Prohibited Transaction rules, a central problem for many business owners looking to shift future growth of their business into their retirement account is that they need to be able to find someone or some entity – besides themselves (which can never happen) – from which their IRA can purchase the interest in the business. That means not just finding any willing seller (which may be difficult, because if the business has substantial growth potential, other owners may not be interested in selling!), but a willing seller from whom the business owner’s IRA can legally purchase such an interest without also causing a Prohibited Transaction.

Many entrepreneurs and successful business owners own 100% of their business, especially in early, high-growth years. Given the Prohibited Transaction rules discussed above, there is no way for such individuals to purchase a portion of the business with their IRA. In short, there is simply no one else available that the IRA even could be able to buy shares from!

As again, recall that an individual is always a Disqualified Person with respect to their own IRA. As such, if such an individual owns 100% of the company, the only two places from which a portion of the company could be purchased – by anyone, or any entity, including the individual’s own IRA – is from the individual themselves (by selling their shares to the IRA), or the company itself (via the issuance of new shares, units, etc.), both of which are Disqualified Persons.

In many other situations, a small business will be owned entirely by a small group of close family members. The end result, in such cases, is precisely the same, because the IRA owner’s spouse, ancestors (parents and grandparents) or lineal descendants (children and grandchildren) are also Disqualified Persons.

Accordingly, the first step for business owners looking to purchase additional interests in the business with their IRA money is to ensure that there are actually interests that can be purchased with those funds!

Transferring shares when Disqualified Persons own 50% of more of outstanding shares

When it comes to the Prohibited Transactions rules, the sad and frustrating reality is that while there are situations in which the rules clearly allow, or don’t allow, a particular transaction, there is often an extraordinary broad gray area, in which a transaction may (or may not) be a Prohibited Transaction. One such gray area is the treatment of a business that is already owned 50% or more by Disqualified Persons.

There is no doubt that the 50% threshold definitely removes additional owners from the pool of potential sellers to the IRA belonging to the 50% or greater owner (along with related Disqualified Persons). Specifically, as detailed above, once the 50% threshold is met (where 50% or more of outstanding shares are owned by a Disqualified Person), the business, itself, becomes a Disqualified Person, as does any 10%-or-more owner of that business, employee earning 10% or more of the wages of that business, or officer, director or person with similar responsibilities of that business.

But what if there are other, non-disqualified persons willing to sell their interests in the business to the IRA of an already-50% owner (personally)? That’s where things get murky. Some experts believe that the 50% ownership of the business directly by the individual makes the business ‘uninvestable’ by the Disqualified Person’s IRA. On the other hand, other experts believe that even though the company, itself, would be a Disqualified Person if it were directly owned 50% or more by the IRA owner (and related Disqualified Persons), if the IRA can find a non-Disqualified Person from which to buy additional interests from, the actual transaction (purchase) would be with a non-Disqualified Person and, therefore, could be permissible.

On the surface, that would seem to make sense, as the Prohibited Transaction rules are designed to prevent individuals from unfair usage of tax-preferenced accounts, and an unrelated third party would have no incentive to sell their portion of the business to the IRA at anything less than ‘full’ price (and without any other ‘family’ incentives or similar influences). Nevertheless, even with this latter possibility, where 50% personal ownership doesn’t automatically prohibit the IRA of the same person from purchasing shares from a non-Disqualified Person, there would certainly be an increased risk of the transaction being classified as a Prohibited Transaction due to the more nebulous self-dealing provision under IRC Sections 4975(c)(1)(D), as described further, below.

Ultimately, given the potential ‘cost’ of being wrong – the immediate and full distribution of an individual’s entire IRA account – it would seem that, in general, individuals would be best served with a ‘better safe than sorry’ approach.

Self-dealing and buying shares with <50% ownership

And what about situations in which an IRA owner and related Disqualified Persons own less than 50% of a business? Is the individual’s IRA free to invest in the business in such a situation with impunity?

Unfortunately, the answer here is “no,” thanks in large part to IRC Section 4975(c)(1)(D)’s restriction on the “transfer to, or use by or for the benefit of, a disqualified person of the income or assets of a plan.” Essentially, this provision of the Internal Revenue Code asks the subjective question, “Was the IRA investment made to benefit the IRA owner personally in any way?” (outside of their IRA growing in value).

The answer to this question, which explores so-called “self-dealing,” is somewhat in the eye of the beholder. Perhaps not surprising then, case precedent and Department of Labor Opinion Letters (requests from taxpayers to the Department of Labor to determine whether a proposed or actual transaction would constitute a Prohibited Transaction) are incredibly inconsistent.

Consider, for instance, the facts outlined in Technical Advice Memorandum (TAM) 9119002, where the owner of a retirement account lent money from his retirement account to a company of which he was a 39% owner. Given the individual’s ownership of the company was less than 50%, the company was not, by rule, a Disqualified Person.

And yet, in the IRS’s view, the loan was a prohibited transaction. Specifically, the IRS reasoned that since the individual was such a significant owner of the company, the company’s securing of the loan would be of benefit to him personally. Thus, the loan constituted self-dealing and a Prohibited Transaction.

About the only thing that can be said definitively here, is that the less of a company an individual owns personally, and the more distant the relationship between an individual and the counterparty of a transaction with their IRA, the less of a problem they will have buying additional ownership in the company via their IRA from non-Disqualified Persons. Conversely, the greater the personal ownership, and/or the closer the relationship between an individual and the counterparty of a transaction with their IRA, the greater the risk that the purchase of additional ownership interests via an IRA – even from a non-Disqualified Person – would, upon examination (audit), result in a self-dealing Prohibited Transaction.

Accordingly, individuals with (for example) 49% personal ownership in a business should probably not use their IRA to purchase additional amounts. By contrast, individuals with 1% personal ownership can probably buy additional amounts in their IRA with minimal concern. As for where the breakeven point in between is? That’s best left up to the client’s tolerance for audit risk, ‘fighting’ with the IRS, and the advice of qualified tax and legal counsel.

Shares should be purchased at fair market value

Regardless of how much of a business an individual owns personally, if/when shares are purchased with their IRA, they should be purchased at fair market value. In short, the IRA should purchase shares at the same price that would be offered to anyone else. As while selling shares at fair market value is not a safe harbor to transact with a Disqualified Person (so even at fair market value, IRAs cannot purchase shares from a Disqualified Person), when purchasing from a non-Disqualified Person, transactions with an IRA must still be conducted at fair market value.

As in practice, shifting value into retirement accounts by artificially suppressing the value of business assets at the time of purchase has long been on the IRS’s radar. In fact, in 2004, the IRS released Notice 2004-8, Abusive Roth Transactions, in which it added value-shifting techniques to its “Listed Transactions.”

This classification is important, because not only do taxpayers have a responsibility to proactively notify the IRS when they engage in Listed Transactions (and for which there are substantial penalties for non-compliance), but if deemed to be a value-shifting move, the excess value (beyond fair market value) ‘stuffed’ into the retirement account can be treated as an excess contribution. Such contributions are subject to a 6% penalty, per year, until removed.

Putting 100% of a new business into a Roth IRA

Purchasing an existing business with IRA funds is one thing, but what if an individual has a new idea for a business that is “guaranteed” to ‘explode.’ Can they start that business within their IRA?

The answer – with a whole laundry list of caveats – is yes. In fact, the individual’s Roth IRA can even become the 100% shareholder of the business!

But how?

It all comes down to a nuanced reading of the Prohibited Transaction rules. More specifically, while a company in which an individual owns 50% or more of the interest is considered a Disqualified Person, prior to the formation and capitalization of the company, it has no owners. Thus, the company cannot yet be a Disqualified Person!

While this may sound like a bit of an end-around, the concept has been repeatedly ‘blessed’ by the Tax Court, beginning with the Swanson case in 1996. In that case, the Court stated:

“A corporation without shares or shareholders does not fit within the definition of a disqualified person under section 4975(e)(2)(G). It was only after Worldwide issued its stock to IRA #1 that petitioner held a beneficial interest in Worldwide’s stock, thereby causing Worldwide to become a disqualified person under section 4975(e)(2)(G).” [Emphasis added]

The Tax Court’s logic has since been reaffirmed in a variety of cases. Accordingly, taxpayers are on solid ground creating a new company, and having their Roth IRA become the owner of some, a majority, or even the entire company (by issuing shares in the newly formed company directly to the retirement account, in exchange for an initial contribution to the entity, when the company is established).

But that doesn’t mean IRA owners are totally in the clear with respect to Inhibited Transactions and such investments. Rather, there’s still plenty of opportunities for such individuals to err.

Receiving (prohibited) personal compensation from an IRA-owned company

One complication for entrepreneurs when their IRA (along with the IRAs of other related Disqualified Persons) exercises control over a business, is that they are no longer able to receive compensation personally from that business. As the IRA owner receiving compensation individually, via a company owned by the IRA (and a company which the IRA owner still indirectly controls by their ownership of the IRA), could run afoul of several separate Prohibited Transactions, including the above-referenced “for the benefit of” a Disqualified Person rule under IRC Section 4975(c)(1)(D), and IRC Section 4975(c)(1)(F)’s limitation against a Disqualified Person who is also a fiduciary’s (which includes an IRA owner) receipt of “any consideration for his own personal account.”

Case in point: In a 2013 court case, Ellis V. Commissioner (TC Memo 2013-245), Ellis decided to use his IRA to purchase 98% of a newly formed LLC (while the other 2% was owned by an unrelated individual). While the IRS initially tried to ‘attack’ that purchase as a Prohibited Transaction on its own, the Court determined (relying on the Swanson decision, as noted earlier) that the initial purchase by Ellis’ IRA didnot constitute a Prohibited Transaction.

Unfortunately, while Ellis ‘escaped’ the wrath of a deemed Prohibited Transaction there, his subsequent actions, after the business was established and owned (mostly) by his IRA, doomed him. Specifically, Ellis paid himself compensation (personally) from the business owned by his IRA, and for which he worked. The Court found this action to constitute a Prohibited Transaction.

From the Court in the Ellis decision:

“As the fiduciary of his IRA—a member of CST with 98% of the outstanding ownership interest—and the general manager of CST, Mr. Ellis ultimately had discretionary authority to determine the amount of his compensation and effect its issuance in either circumstance.”

“In causing CST to pay him compensation, Mr. Ellis engaged in the transfer of plan income or assets for his own benefit in violation of section 4975(c)(1)(D). Furthermore, in authorizing and effecting this transfer, Mr. Ellis dealt with the income or assets of his IRA for his own interest or for his own account in violation of section 4975(c)(1)(E).” [Emphasis added]

In other words, the Court determined that because Ellis controlled his IRA that owned the business, and furthermore was the general manager of the business, he had the ability to compel the IRA-owned business to pay whatever he wanted to himself, effectively dealing IRA assets to himself through the business as a conduit, which is unequivocally a Prohibited Transaction.

Receiving compensation from a business only partially IRA-owned

As noted above in the emphasized portions of the excerpts from the Ellis case, the control Ellis had over the business – both due to his majority ownership via the IRA and his managerial authority within the business – caused a Prohibited Transaction to occur once he paid himself.

In situations where an IRA owner does not own a majority of the company they work for via their IRA (the IRA owns less than 50%), and in which they do not exercise control over their employment and/or compensation (the IRA owner is not in a position of authority to set their own compensation), the outcome is less certain. Without control (whether by ownership or management), an individual can potentially receive compensation from a business that is partially owned by their IRA without triggering a prohibited transaction.

From a practical perspective, the fact that a lack of control (by ownership or management) is sufficient insulation to avoid a Prohibited Transaction is why an IRA can own a publicly traded company, and employees of that company generally do not need to worry about a Prohibited Transaction even if they work for (and are compensated via) a company that their IRA owns.

However, as either the relative ownership of the IRA rises (as in the case of a publicly traded firm, the typical IRA would still only own a minuscule fraction of 1% of shares, but privately held companies could own far more), or the relative management role of the IRA owner increases (e.g., the IRA-owned business appoints the IRA owner into a senior management/leadership role), if the IRS determines that the individual’s IRA investment has any influence over the IRA owner’s compensation (or their outright employment at the company altogether), the compensation could still give rise to a Prohibited Transaction.

Contributions of ‘sweat equity’ can create prohibited transactions

For some wealthier entrepreneurs of means, the inability to receive compensation from investments owned in large part (or entirely) by their Roth IRA would not be a problem. Indeed, if such an individual has enough income and/or assets with which to fund their ongoing expenses, not receiving compensation from such a company would likely be in their best interest, as it would allow more profits to accumulate tax-deferred within their retirement account (or alternatively to be reinvested into the business for faster growth).

A lack of direct compensation (compensation paid to the individual, personally) from a company owned 50% or more by an individual’s IRA does not, however, give that individual free rein to work within the company without fear of implicating the Prohibited Transaction rules.

Rather, contributions of ‘sweat equity’ could be considered an impermissible furnishing of services, and a Prohibited Transaction, under IRC Section 4975(c)(1)(C)’s prohibition of the ‘furnishing of goods, services, or facilities between a plan and a disqualified person.” [Emphasis added]

Example #4: Old McDonald recently used his IRA to buy 100% of a newly created company, OMDF, LLC. Using the money contributed to OMDF by Old McDonald’s IRA, OMDF purchased a farm.

Having worked as a farmer for most of his life, Old McDonald wants to put his skills and experience to use working in the field with the rest of the IRA-owned OMDF’s farm employees. Unfortunately, though, Old McDonald cannot do so without creating a Prohibited Transaction.

Since the farm is ultimately owned by Old McDonald IRA, and Old McDonald, as the owner of that IRA, is a Disqualified Person, working the field would be a clear-cut example of the furnishing of services between a plan and a Disqualified Person.

Permissible actions by an IRA owner on behalf of an IRA-owned business

Although, as discussed above, an IRA owner is prohibited from providing ‘sweat equity’ to a business that is controlled by their IRA, that doesn’t mean they need to be completely hands-off from the business. Rather, such individuals can perform a variety of functions, provided they are more administrative or managerial in nature.

An IRA owner can, for instance, be responsible for paying expenses of an IRA-owned business using the funds of that IRA-owned business. In other words, while the IRA owner can’t use their own personal assets to pay for the IRA-owned business’s expenses, they can be the person in charge of physically writing out checks from the IRA-owned business’s bank account (or ‘clicking the button’ to pay the business’s bills electronically). Similarly, the IRA owner can physically receive payments made payable to the IRA-owned business and deposit them into the IRA-owned business’s account.

Furthermore, the IRA owner can make managerial decisions on behalf of the business. Such decisions could include decisions on hiring and firing employees and contractors, signing agreements with vendors, and authorizing the IRA-owned business’s own investment activities (such as authorizing an IRA-owned manufacturing business to purchase a new piece of machinery).

Ultimately, it is the more direct ‘provision of services to’ the business (doing the work of the business itself), as opposed to performing actions of the business, by the IRA owner that most directly implicates the Prohibited Transaction rules for an IRA-owned business.

IRAs represent one of the most widely available tax shelters to the typical taxpayer. Notably, the tax-deferred growth enjoyed by IRAs increases in value as the returns of the account increase. Accordingly, individuals often try to shift highly appreciating assets into their retirement accounts, and in particular, Roth-style retirement accounts, where all future growth will be tax-free.

For most taxpayers, there is a large enough selection of ‘traditional’ investments, such as stocks, bonds, mutual funds, and ETFs, that exploring other, more complex assets is neither necessary nor desirable. For other individuals, less traditional investments offer the promise of potentially greater returns.

Entrepreneurs and small business owners, in particular, are often extremely bullish on their businesses (that’s why they started/bought them in the first place), and from time to time, express interest in using their retirement accounts to purchase some or all of their businesses to benefit from both the businesses perceived high growth rate and the IRA’s tax benefits.

In some instances, such an investment is possible. However, using an IRA to invest in a business that is already owned (in part) personally by the IRA owner and/or other Disqualified Persons can be fraught with challenges. Any business interests acquired by an IRA, for instance, can never be purchased directly from the IRA owner or other Disqualified Persons.

Furthermore, even if an individual is able to use their IRA to purchase an interest in a business, they must comply with other Prohibited Transactions rules as the business is being operated. This can restrict both the compensation that can be paid directly to the individual, as well as the types of activities that they may be able to perform on behalf of the business.

Ultimately, the key point is that while IRAs can invest in anything other than life insurance, collectibles, and S corporation stock, the Prohibited Transaction rules can complicate matters when desired investments include privately held businesses in which the IRA owner also owns a personal interest and/or for which the IRA owner provides services.

Jeffrey Levine, CPA/PFS, CFP, MSA, a Financial Planning contributing writer, is the lead financial planning nerd at Kitces.com, and director of advanced planning for Buckingham Wealth Partners.